These days several retailers offer buy now, pay later plans that allow consumers to make purchases without paying in full up-front. While the appeal is great, there are a few key things you should know before agreeing to these types of plans. You may end up paying more than expected. Check out how these plans work and what to look out for before saying yes to buy now pay later plans.

How Buy Now, Pay Later Plans Work

As mentioned in the introduction, buy now pay later plans allow customers to make purchases without paying in full right away. These plans are often called “installment” or “pay over time” plans.

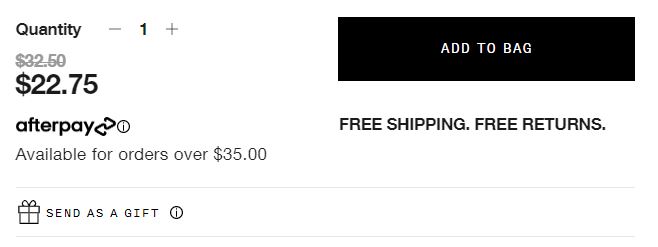

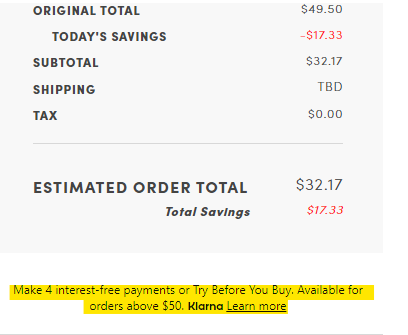

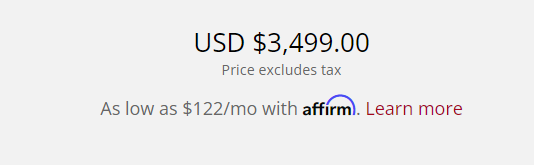

With these types of plans you initially pay a portion of the cost to get the product. That money is sent to the company that manages the plan. That company pays the retailer in full and over time you pay the remaining payments to the company that manages the plan. For example, Klarna, AfterPay, and Affirm are some of the top buy now, pay later providers that offer payment options to various retailers nationwide. Some plans may require a credit check to determine eligibility, but not all.

While many of these plans advertise “no-interest payments” and “few or no fees”, the reality is they do charge fees, sometimes high fees at that. Some fees that may be charged include:

- transaction fees for each payment

- late fees

- payment date modification fees

In addition, if you set up autopay and do not have enough funds to cover the payment, you can be hit with overdraft fees from the bank.

Be aware that some of these companies report your payments to the three main credit bureaus (Equifax, Experian, and TransUnion). Making payments on time may improve your credit. Any missed or late payments can harm your credit score.

What to Consider Before Choosing a Payment Plan

Buy now, pay later options may sound like a good idea, but be aware it could cost you more in the end. Never give in to high-pressure sales tactics. Take some time to go over the agreement and ask any questions you may have so you understand your obligations. Do your research. Start by looking up the company on www.checkbca.org. Also, search the internet for consumer reviews and complaints regarding the service.

Understand that the company that manages the payment plan for buy now, pay later transactions is not the same as the retailer. If you have problems with your purchase, the payment plan monitor will more than likely be unable to assist you. Keep in mind that scammers are using these payment plan options in their ruse. Checkout BCA’s exposé on a recent scam that used AfterPay to con its victims.

Getting Help with Fraud

Check with your state attorney general or state and local consumer protection agencies for more information on laws that may apply to buy now, pay later plans and your rights when you use these plans. If you run into a problem, file a complaint with BCA and we will reach out to the company for a response. You can also contact the Federal Trade Commission (FTC) at ReportFraud.ftc.gov.

Follow Business Consumer Alliance on Facebook for trending information, scam alerts, and more.